Financing a property in Switzerland requires thorough preparation and careful planning. Success depends on many factors, including choosing the right financing models, obtaining the right documentation and comparing loan offers. In this article, we offer you a comprehensive guide to systematically approaching your real estate financing and ensuring that you invest securely and for the long term.

Preparations for real estate financing

Before you start financing, you should obtain a credit report from the Central Office for Credit Information (ZEK). This will give you and your potential lender an overview of your financial reliability. Correct any errors in your credit report to increase your chances of being granted a loan.

The first step in financing your property is to calculate the purchase price of the property and calculate the ancillary costs. Incidental costs include notary fees, transfer taxes and any estate agent fees. Also think about future renovation or modernization costs that need to be taken into account.

Equity and mortgage models

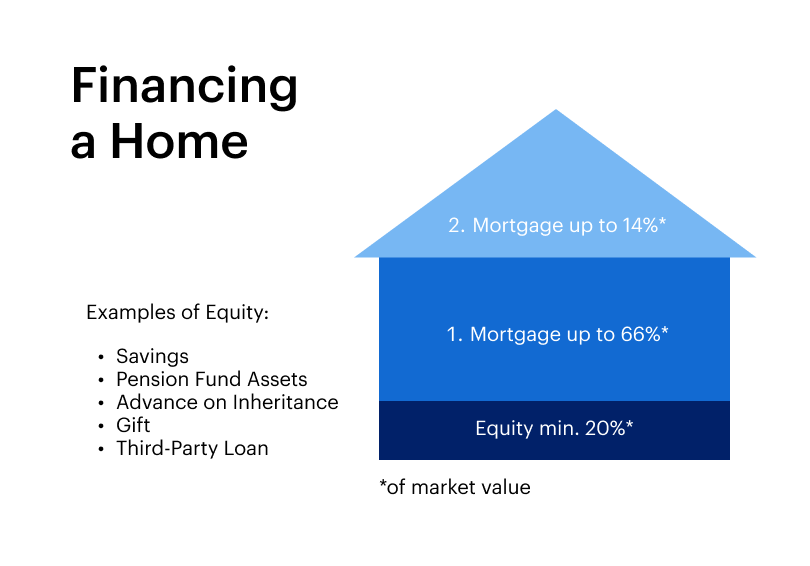

Own funds, also known as equity, comprise the capital that a buyer puts up themselves to finance a property. These assets flow into the purchase process in addition to the mortgage. In Switzerland, equity capital requirements are high: at least 20% of the purchase price should come from the buyer’s own funds, of which at least 10% should come from own funds.

The higher your equity, the more favorable the loan conditions can be. Therefore, check your financial reserves and consider how much of them you can contribute to the real estate financing.

There are various mortgage models that differ in terms of interest rate and flexibility. A fixed-rate mortgage offers stable interest rates over a fixed term, while Libor and variable-rate mortgages offer more flexible but riskier conditions. Choosing the right model depends on your financial situation and your risk tolerance.

Comparison of credit offers

Comparing interest rates and loan conditions is essential in order to identify the best offers. Pay attention to the effective interest rate, the term of the mortgage, the amortization plans and possible special repayment options. The total cost of the loan should also be taken into account. Mortgage providers in Switzerland include banks, insurance companies, pension funds and online platforms. Each of these options can offer different benefits, so it’s worth getting several quotes and comparing them carefully.

At properti, we place great importance on offering our customers the best conditions for their property financing. Through close cooperation with our financial partners, we can offer the best terms. With properti to the mortgage. Request now

Applying for the loan

Complete and correct documentation speeds up the loan application process. Collect proof of income, proof of equity, the exposé of the property, the purchase contract or the purchase commitment as well as other required documents such as land register extracts and site plans. A well-prepared loan application increases your chances of a positive loan decision. Clarify all open questions with your loan advisor and submit the complete documents.

Amortization

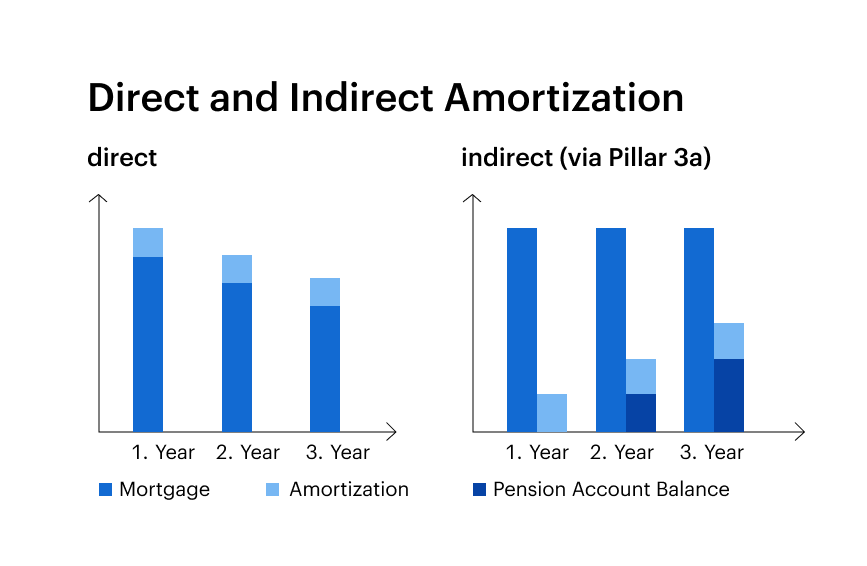

Amortization, i.e. the repayment of the mortgage in instalments, is a crucial aspect of real estate financing. In Switzerland, the mortgage must usually be repaid within 15 years at 65% of the house value to ensure affordability in old age. There are two types of amortization: direct and indirect. With direct amortization, you pay back a fixed amount to the bank each year, which means that your debt and interest charges fall continuously. With indirect amortization, the payments are placed in a pension account (e.g. pillar 3a), which serves as security for the mortgage. This method offers tax advantages, as the payments are deductible, and also allows full tax deduction of the mortgage interest.

Protection through insurance

Buildings insurance is compulsory in Switzerland and protects against damage caused by fire and natural hazards. Life insurance can be particularly important in the case of indirect amortization to protect your surviving dependents. Additional insurance policies such as disability insurance or residual debt insurance offer further protection and can cover financial risks in the event of incapacity to work, illness or death.

Notary fees and other fees

Notary fees are incurred for the notarization of the purchase contract and entry in the land register. These costs vary from canton to canton and should be taken into account in your financial planning. Transfer taxes are regulated differently from canton to canton and are usually borne by the buyer. However, a different distribution of costs can also be agreed in the purchase contract. Also check any estate agent commissions and fees for obtaining documents.

Completion of financing and financial management

Check the loan agreement thoroughly for correctness and completeness. Ask your lender to explain any unanswered questions to avoid any misunderstandings. Once the loan agreement has been signed, the loan will be paid out. Make sure that all payment deadlines are met and monitor the entire process carefully.

After completing the financing, it is important to plan the monthly installments into your budget and monitor your financial obligations. Keep track of your expenses and regularly review your financial situation. If necessary, take advantage of the option to make an unscheduled repayment or reschedule your debt to further improve your financial situation.

Conclusion

Careful planning and a systematic approach are crucial for successful real estate financing in Switzerland. Use the tips above to structure your financing securely and for the long term. If necessary, consult experienced advisors to avoid problems and keep track of costs. This way, nothing stands in the way of your dream of owning your own property.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.