|

Getting your Trinity Audio player ready...

|

Key facts:

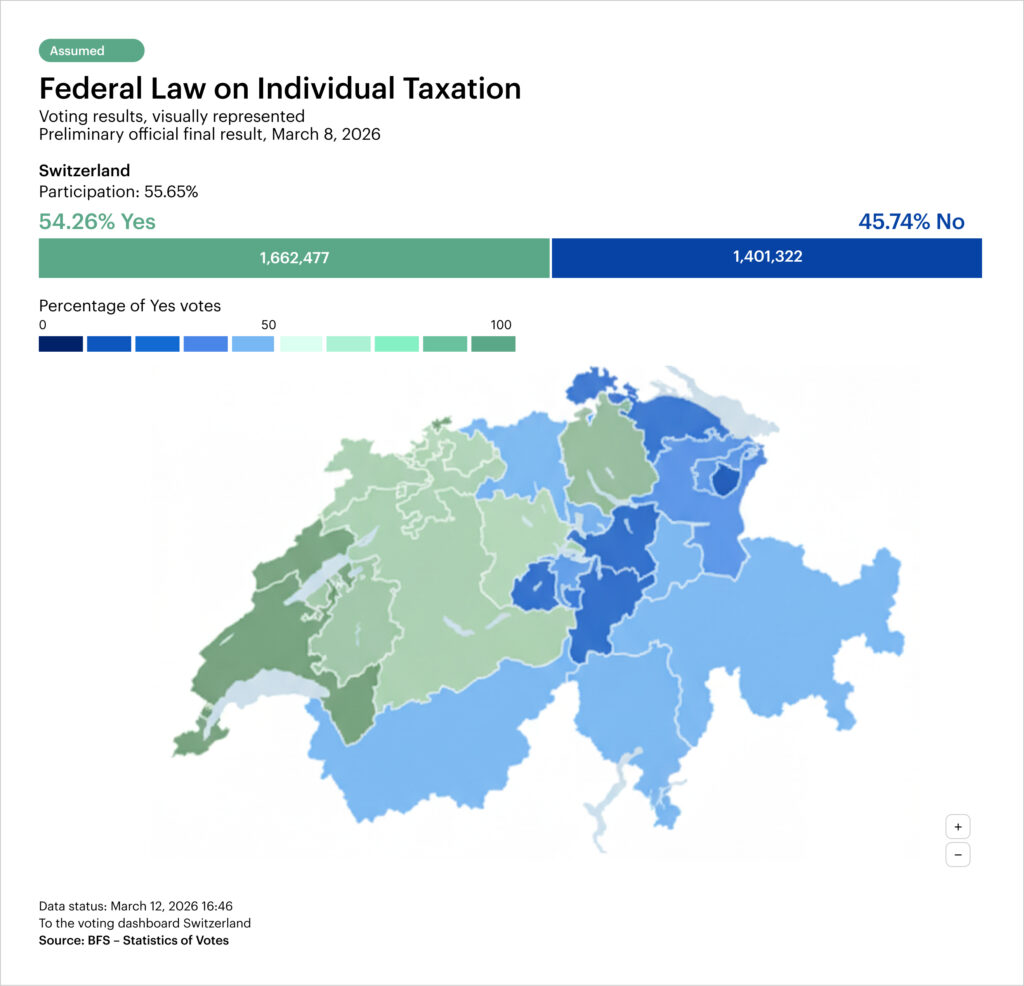

- On March 8, 2026, Switzerland adopted individual taxation in a referendum.

- By 2032 at the latest, everyone will pay tax on their income and assets regardless of their marital status.

- In future, real estate will be divided up for tax purposes according to the owners’ share in the land register.

On March 8, 2026, the Swiss population approved the Federal Act on Individual Taxation. In future, every taxable person will pay tax on their income and assets regardless of their marital status. This marks the end of the previous system of joint taxation for married couples.

A historic system change in the Swiss tax system

The reform applies to the federal government, cantons and municipalities. The cantons must adapt their tax laws accordingly. The new system will come into full force by 2032 at the latest, although an earlier date is possible.

Individual taxation is regarded as one of the biggest tax policy reforms of recent decades. It affects not only income and assets, but also key areas such as home ownership, mortgages and asset structuring.

This raises a key question for owners and buyers: What impact will individual taxation have on the real estate market in Switzerland?

What exactly will change with individual taxation?

The reform applies to the federal government, cantons and municipalities. The cantons must adapt their tax laws accordingly. The new system will come into full force by 2032 at the latest, although an earlier date is possible.

- Taxation irrespective of marital status

The reform completely realigns the tax principle.

In the future:

- Each person submits a separate tax return.

- Income and assets are taxed individually.

- The same tax rate applies to married and unmarried persons.

This abolishes the so-called marriage penalty in tax law.

- Assets, income and real estate are allocated individually

A central point of the reform concerns the allocation of assets. In principle, the principle of civil law ownership will apply in future:

- Assets are attributed to the person to whom they legally belong

- Joint bank accounts are generally divided equally

- The recipient pays tax on pensions or lump-sum withdrawals from the pension fund and pillar 3a

Debts and mortgages are now also clearly allocated, as they are credited for tax purposes to the person listed as the debtor in the loan agreement. Regardless of who actually pays the interest.

- Residential property is taxed according to land register share

The new regulation is particularly relevant for property owners, as taxation will in future be based strictly on the land register entry: if only one person owns the property, they will pay tax on it alone; in the case of joint ownership, taxation will be based on the ownership ratio.

This applies in particular to imputed rental value, property tax and debt interest deductions. This will make the tax treatment of real estate much more transparent and individual.

What impact does individual taxation have on the real estate market?

1. more transparency in ownership structures

The reform strengthens the importance of clear ownership structures.

For real estate, this means

- Ownership shares in the land register gain importance for tax purposes

- Mortgage agreements and debtor structure are becoming more relevant

- Wealth planning becomes more individual

Particularly in the case of jointly acquired residential property, an exact division of ownership shares could be carried out more frequently in future.

2. changes in the tax planning of real estate

For many households, real estate planning is becoming more complex, but at the same time more flexible.

Possible developments:

- Greater tax optimization of ownership interests

- More targeted use of debt interest deductions

- Individual asset structuring within couples

Tax structuring is particularly important for larger real estate assets or multiple properties.

3. new dynamics for second earners and home ownership

In the long term, the abolition of joint taxation could also have an impact on employment incentives within households.

Economists expect higher employment among second earners and rising household incomes in certain segments. This could improve the financing options for home ownership, particularly in urban regions with high demand.

What owners should consider now

Even if the reform will not be fully implemented for several years, it is worth taking a look at the possible consequences today. An early analysis can be particularly useful for properties with a high value or multiple owners.

These are particularly relevant:

- Ownership structure in the land register

- Mortgage agreements and debtor rolls

- Long-term tax planning

Conclusion: Individual taxation brings more individuality – also for real estate

The introduction of individual taxation is fundamentally changing the tax logic in Switzerland. For the real estate market, the allocation of assets, the ownership structure in the land register and the structure of mortgages will come more into focus. In the short term, the reform is unlikely to change market activity. In the medium term, however, tax planning for residential property will become more important. It will therefore become more important for owners to review their own real estate strategy at an early stage.

FAQs

When does individual taxation come into force?

The law will come into force in 2032 at the latest. Cantons must adapt their tax laws and tariffs before then.

Will married couples have to submit two tax returns in future?

Yes. With the reform, each person will submit a separate tax return in future. For married couples, this means that income, assets, debts and deductible items will in future be declared individually and allocated according to the ownership and contractual relationships under civil law. Particularly in the case of residential property, mortgages or joint accounts, the tax division can thus become clearer, but also more challenging in practice.

How will residential property be taxed in future?

Taxation is based on the land register entry. In the case of joint ownership, the property is taxed pro rata according to the ownership share.

Will the reform have an immediate impact on the real estate market?

No major market changes are expected in the short term, as the new law will not come into force until 2032 at the latest and the current system will apply until then. The direct effects will mainly affect tax planning, the ownership structure and the future structure of property ownership within couples.

Does the individual taxation reform also affect mortgages?

Yes. In future, debt interest will be credited for tax purposes to the person who is registered as the debtor in the mortgage agreement. This will make the contractual structure of mortgages more relevant for tax purposes, particularly in the case of jointly financed residential property or unevenly distributed debtor roles within a partnership.