Key facts:

- Key interest rate lowered to 0.50%: The SNB’s decision provides positive impetus for the real estate market and lowers financing costs.

- Focus on mortgage interest rates: cheaper mortgages could increase demand for real estate, while experts warn of overheating.

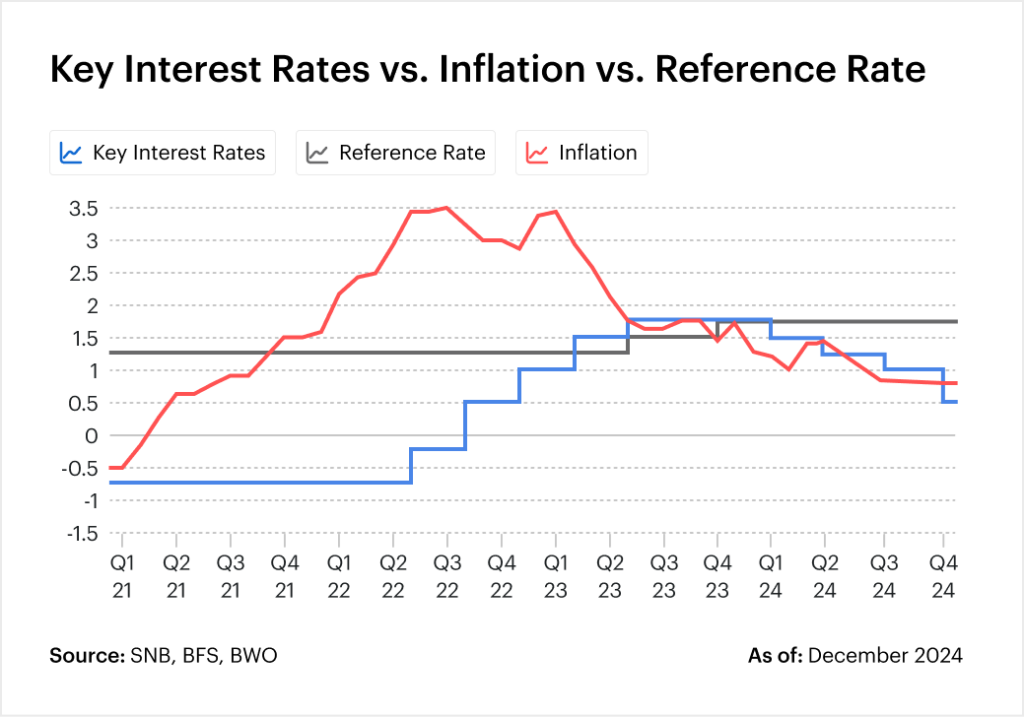

A strong signal – The Swiss National Bank’s (SNB) reduction of the key interest rate by 0.5 percentage points to 0.5% creates new growth impetus for the real estate market. A sustained period of low interest rates could not only stimulate the market, but also lead to lower mortgage and rental rates. This development offers potential for sustainable growth and relief for many tenants. But what does this mean in concrete terms?

What impact will the key interest rate cut have on the real estate market?

The SNB’s interest rate cut is providing positive impetus for the real estate market. It influences financing options, rental prices and market dynamics – opportunities and challenges for everyone involved.

1. mortgage interest

With the cut in the prime rate, mortgage interest rates are likely to fall further, making real estate purchases more affordable. However, the high demand could push up property prices further. Experts therefore advise caution in order to counteract a possible overheating of the market.

2. rental prices

A falling key interest rate has the potential to lower the mortgage reference interest rate in the medium term. If this is adjusted, rents could fall. The reference interest rate currently stands at 1.75%; an adjustment could take place in March 2025 at the earliest.

3. market dynamics

The SNB’s interest rate policy could accelerate the momentum on the real estate market: While buyers benefit from better financing options, supply could become tighter. Lower interest rates in turn encourage new construction, which could increase supply in the medium term. Nevertheless, the realization of new projects remains challenging due to high construction costs and regulatory requirements.

What impact will the key interest rate cut have on buying, selling and renting real estate?

The key interest rate cut not only affects the real estate market as a whole, but also has a concrete impact on buying, selling and renting. Depending on the perspective, new opportunities arise, but also challenges that require strategic action.

- Purchase

For buyers, the lower mortgage interest rates open up attractive financing options. This reduces monthly charges, which attracts first-time buyers and investors in particular to the market. This leads to increased demand and rising property prices. In the long term, buyers can benefit from the opportunity to secure favorable interest rates, which offers them more planning security.

- Sales

On the seller side, the increased demand makes it more likely that properties will sell faster and at higher prices. The shortage of sought-after properties is driving prices up further, allowing sellers attractive margins. Especially in urban and sought-after locations, sellers can benefit from these developments and take advantage of the right time to sell their properties at a profit.

- Rent

There is a different dynamic for tenants. Rising property prices, steady population growth and scarce availability in sought-after regions could drive rents up further, as the supply of rental apartments is limited in many urban centers. At the same time, the favorable financing conditions encourage the construction of new rental apartments, which could increase supply and reduce pressure on rents in the long term. A possible adjustment of the reference interest rate next year could bring relief.

Outlook: What’s next?

Overall, the key interest rate cut is acting as a catalyst for the real estate market. It is boosting demand, strengthening the position of sellers and increasing the pressure on tenants. Nevertheless, the long-term development remains dependent on other regional and economic factors. Experts expect interest rates to remain at this level or could even fall further if inflation remains low and the economic conditions require it. Buyers and sellers should be prepared for a dynamic development.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.