|

Getting your Trinity Audio player ready...

|

Key facts:

- The SNB confirms the key interest rate at 0% on September 25, 2025.

- Mortgages remain attractive, but banks continue to expect 4.5-5% affordability.

- Buyers benefit from favorable financing, owners from high demand.

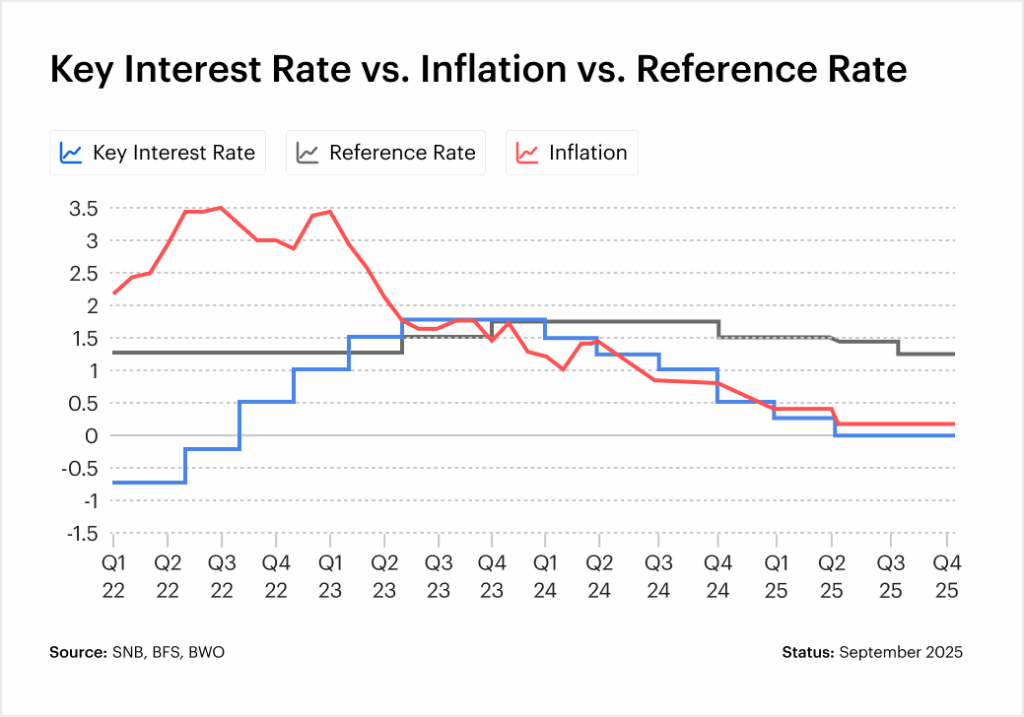

On September 25, 2025, the Swiss National Bank (SNB) decided to leave the key interest rate unchanged at 0.00%. A reduction had already been made in June, and the SNB is now focusing on stability. For the real estate market, this decision primarily means planning security. Owners and buyers can assume that financing costs will remain at a favourable level in the coming months – an important basis in an environment that continues to be characterized by high demand and tighter supply.

Why the SNB is sticking to interest rates

The decision not to lower the key interest rate any further is based on several factors. Firstly, a return to negative interest rates in the current geopolitical environment could be interpreted as currency manipulation and weaken Switzerland’s position in the trade conflict with the USA. Secondly, inflation is stable at 0.2% in August (core inflation 0.7%), so there is no acute risk of deflation. In addition, the SNB Governing Board emphasizes that the hurdle for renewed negative interest rates is significantly higher today, as their side effects, for example for pension funds and the real estate market, are known from the years 2015 to 2022.

Effects on mortgages

Even if the key interest rate remains at 0.00%, banks will continue to apply strict checks when granting loans. For affordability, institutions continue to expect imputed interest rates of around 4.5-5%. This means that, despite the low market interest rate, buyers must prove that they have sufficient income to obtain financing.

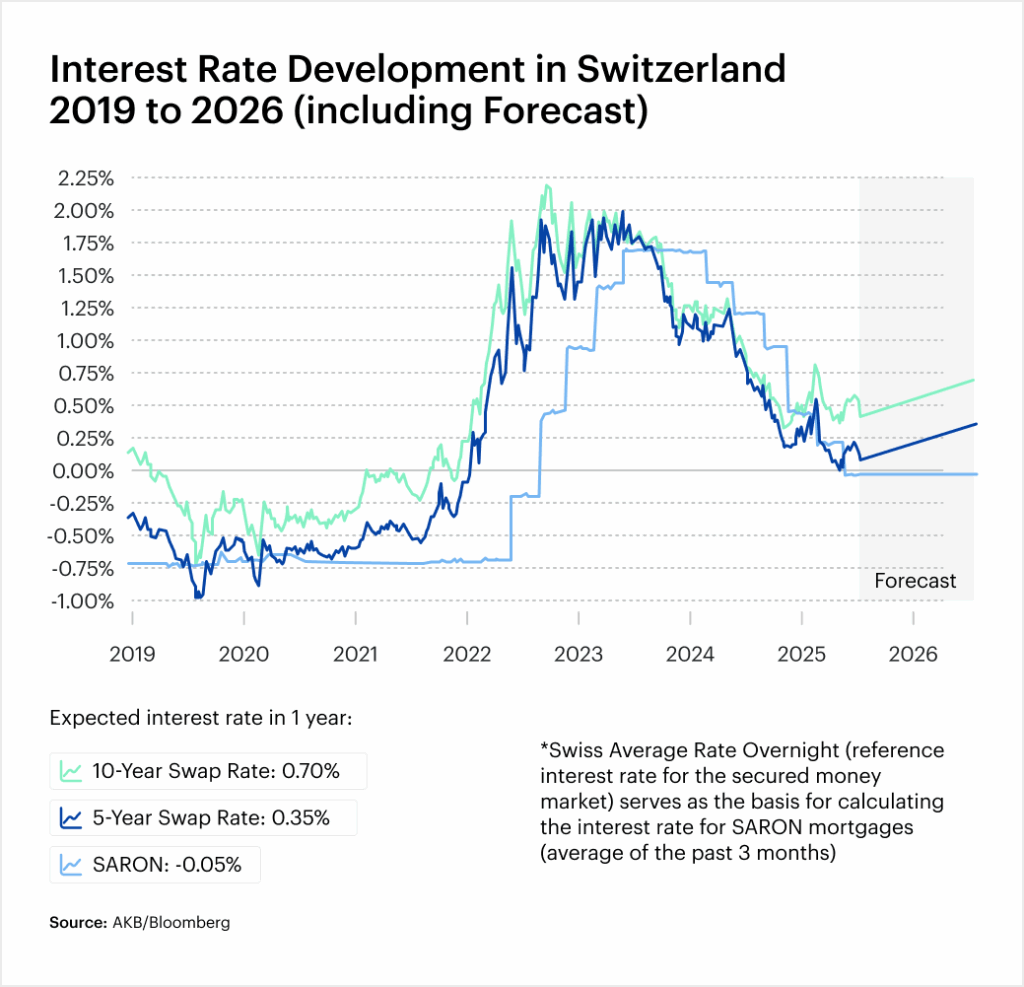

Short-term financing such as SARON mortgages remain close to zero, meaning that the monthly burden for borrowers remains low. However, no significant additional relief is to be expected. Rates for fixed-rate mortgages, which are more closely aligned with the capital market, are already at a low level. Accordingly, hardly any downward movement is expected in the coming months, which means a stable starting position for owners and buyers.

Opportunities for buyers

The environment remains attractive for prospective buyers. The stability of the key interest rate is supporting demand for residential property and creating security for financing decisions. The monthly burden of mortgage interest rates remains low by historical standards. Those who take the plunge into home ownership continue to benefit from favorable conditions, even if access to financing is not easy for everyone.

The pressure on prices could continue, particularly in regions with high demand and limited supply – such as cities or conurbations. As buying is cheaper on average than renting in many places (see Raiffeisen Housing Market Study 2025), home ownership remains an attractive option for many households.

Prospects for owners

Owners can view the SNB’s decision positively. Sales opportunities remain intact, as demand is being supported by buyers. Anyone considering a sale will encounter a market environment that continues to be characterized by high liquidity and attractive financing conditions.

Existing financing also benefits: predictable interest rates ensure that the burden remains stable over a longer period of time. Owners who do not wish to sell at present can benefit from this calm on the market and think about follow-up financing or possible renovations at an early stage.

Conclusion

By maintaining the key interest rate at 0%, the SNB is ensuring stability. For the real estate market, this means Financing costs remain low and demand for residential property remains high. Buyers benefit from favorable loans, owners from a market environment with sustained interest. Those who examine their own situation in good time can make well-founded decisions – whether buying, selling or long-term financial planning.

FAQ

Why has the SNB left the key interest rate at 0%?

The SNB currently sees no need for negative interest rates. Inflation is stable, geopolitical tensions speak against further cuts and the side effects of negative interest rates on pension funds and the real estate market are well known.

What impact does the stable prime rate have on mortgages?

Short-term financing such as SARON mortgages remain favorable, while fixed-rate mortgages are unlikely to fall. Banks continue to calculate affordability at 4.5-5%, which makes financing challenging despite the low market interest rate.

Does the stable prime rate affect savings interest rates and pensions?

Yes, at 0% savings interest rates remain minimal, which makes traditional accounts unattractive. For pension funds and life insurance companies, this means continued pressure on returns, which indirectly supports real estate as a form of investment.

Can the SNB raise the key interest rate again in the future?

In principle, yes. If inflation rises significantly or the economy overheats, the National Bank could raise interest rates. This would result in higher financing costs for property buyers and owners.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.