|

Getting your Trinity Audio player ready...

|

Key facts:

- The SNB policy rate will remain stable at 0% in 2026 and keep short-term mortgage rates low

- Fixed-rate mortgages are increasingly reacting to geopolitical risks and capital market developments

- Medium-term maturities are gaining in importance as they balance costs and planning security

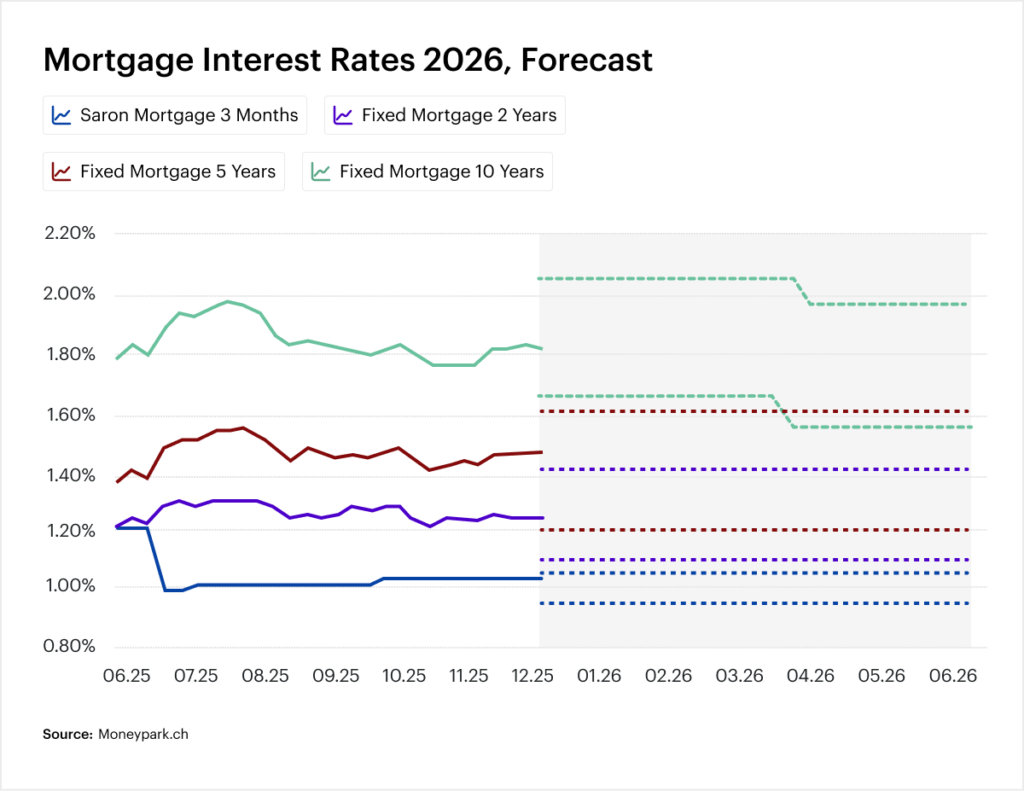

The forecast for mortgage interest rates in Switzerland in 2026 shows a special starting position: while the SNB keeps the key interest rate stable at 0% long-term mortgages are increasingly influenced by global uncertainties, energy prices and capital market movements. For owners, the key interest rate alone is therefore less decisive than the question of which mortgage strategy makes sense in this environment. Those who correctly classify the current market dynamics can manage financing costs in a targeted manner and better hedge risks.

The current situation: Why the SNB is sticking with zero interest rates

Inflation remains at a very low level of around 0.1% at the start of 2026. Forecasts predict around 0.5% in the coming years and thus remain at the lower end of the target range. A key factor is the strong Swiss franc. It reduces imported inflation and stabilizes price trends. This leaves room for maneuver for a supportive monetary policy.

For mortgage borrowers, this means that short-term financing remains attractive.

The Iran conflict and the Strait of Hormuz – Why fixed-rate mortgages are becoming more expensive

In parallel to the stable monetary policy, uncertainty is increasing at a global level. The conflict in the Middle East and the restriction of important energy trading routes – particularly around the Strait of Hormuz as a central hub for global oil transportation – are having a direct impact on the capital markets.

Rising energy prices lead to higher inflation expectations. Investors demand correspondingly higher returns on long-term investments. This is precisely what fixed-rate mortgages are geared towards.

The result is a clear trend: while short-term interest rates remain stable, long-term interest rates are rising or are much more volatile.

SARON vs. fixed-rate mortgage: Which makes more sense in March 2026?

The current yield curve shows a clear picture: the longer the term, the higher the risk premium. In order to make the various models directly comparable, we have summarized the current market situation (forecast March 2026):

| Mortgage | Interest rate | Strategic classification | Risk profile |

| SARON mortgage | 0,70% – 1,30% | Benefit from the stable SNB key interest rate (0%). | High (interest rate risk) |

| 5-year fixed-rate mortgage | 1,00% – 1,60% | The “sweet spot”: Optimal mix of costs & protection. | Medium |

| 10-year fixed-rate mortgage | 1,30% – 2,00% | Focus on maximum security in the face of geopolitical volatility. | Low |

| Green Mortgage | -0.15% to -0.25% | Additional discount for GEAK A/B or Minergie. | N/A |

Sources: Based on the market data and situation assessments of the SNB, ZKB and PostFinance (as at March 2026). The effective conditions depend on individual creditworthiness and property valuation.

This difference makes medium terms particularly attractive. They offer a compromise between planning security and costs. Many owners therefore deliberately opt for 5 to 7 years in order to avoid long-term uncertainties and at the same time ensure stability.

Secure top conditions – the advantage of comparing providers

The differences between financial institutions are considerable in the current market environment. Conditions can vary significantly depending on the provider. Differences of up to 0.5 percentage points are no exception. Over the entire term of a mortgage, this results in considerable savings potential.

A structured comparison thus becomes the basis for all financing. A data-based assessment – such as a property valuation – helps to create the optimal starting position.

Sustainability as a savings factor: how to use green mortgages

Sustainability is increasingly influencing financing costs. Banks are specifically offering better conditions for energy-efficient properties.

Typical advantages:

- Interest rate reductions for GEAK A or B

- Additional bonuses for Minergie standards

- Special environmental loans with temporary discounts

Energy efficiency improvements alone can measurably reduce mortgage interest rates and at the same time stabilize the property value in the long term.

Combining state subsidies and bank bonuses

In addition to bank offers, there are numerous support programs at cantonal and national level. If these are combined, an additional financial lever is created.

This has a double effect for owners:

- Lower financing costs

- Sustainable increase in the value of the property

This aspect is becoming increasingly important, particularly with regard to future regulations.

Conclusion: Mortgage interest rates in 2026 require strategic thinking

Mortgage interest rates in Switzerland will remain stable in 2026 – but only at first glance. While monetary policy ensures calm, the real risks and opportunities arise from global developments and market mechanisms.

For owners, this brings a strategic perspective to the fore. The choice of term, the combination of different models and the integration of sustainability are becoming decisive factors for long-term success.

FAQs on mortgage interest rates in Switzerland 2026

Should a mortgage currently be split up or taken out as an individual solution?

Splitting the loan into several tranches can significantly reduce the risk. By combining SARON and a fixed-rate mortgage, it is possible to take advantage of low short-term interest rates and hedge parts of the financing against future interest rate fluctuations. This strategy is increasingly being used in the current market environment.

When is the right time to refinance?

Refinancing should not be considered just before the existing mortgage expires. It can make sense to secure options as early as 12 to 18 months in advance. Particularly in a volatile environment, there are always favorable time windows that can be used early on.

How does your own life situation influence your choice of mortgage?

The right mortgage structure depends heavily on individual factors such as income, planning horizon or future changes such as retirement or relocation. A long-term fixed rate can offer security, while flexible models are better suited to uncertain phases of life.

What role does affordability play in mortgage lending?

Banks calculate with an imputed interest rate of around 5%, regardless of the current market interest rate. This ensures that the financing remains affordable even if interest rates rise. This rule remains one of the biggest hurdles, especially for first-time buyers.

Is it possible to secure interest for the future today?

Yes, with so-called forward mortgages, current conditions can be fixed up to 18 months in advance. This option is particularly interesting if interest rates are expected to rise or planning security is a priority.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be accepted for the accuracy of the information provided