Key Facts

- Current mortgage situation with low mortgage interest rates in Switzerland.

- Fixed-rate mortgages offer long-term stability, while Saron mortgages guarantee flexibility.

- Expert forecasts point to mixed developments, with possible slight falls in interest rates.

The mortgage landscape in Switzerland has undergone a number of developments in recent years, influenced in particular by the monetary policy decisions of the Swiss National Bank (SNB) and economic conditions. A look at the most common mortgage models – including fixed-rate mortgages, Saron mortgages, variable-rate mortgages and the former Libor 3M – helps to better understand the dynamics and forecasts for future interest rate developments.

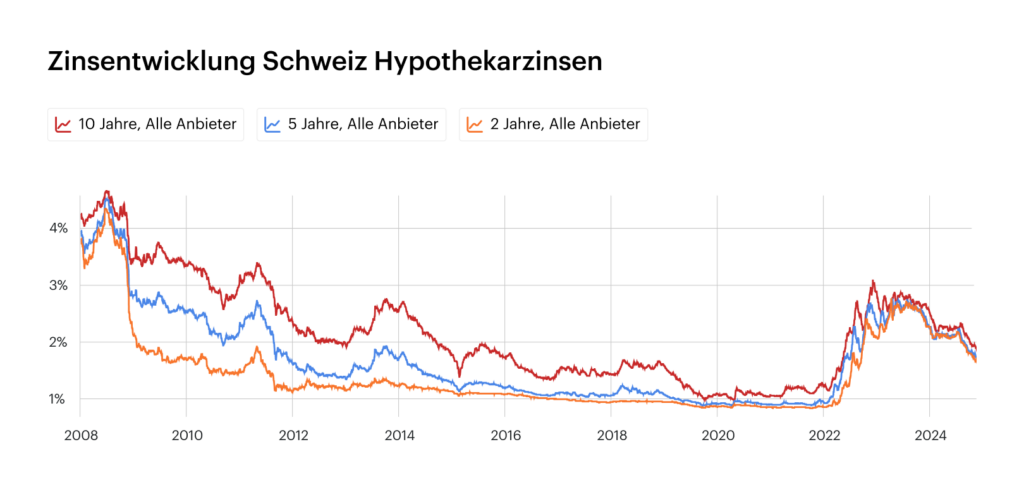

The development of mortgage interest rates and the current mortgage situation

The Swiss National Bank(SNB) has made several adjustments to the key interest rate in recent years in response to economic developments. In June 2022, the SNB raised the key interest rate for the first time in 15 years by 0.5 percentage points to -0.25%. Further increases were made in the following months, bringing the key interest rate to 1.75% in June 2023. In March 2024, the SNB lowered the key interest rate by 0.25 percentage points to 1.5%. This rate cut was the first in several years and was made in response to reduced inflationary pressure and the real appreciation of the Swiss franc. Interest rates were then cut again in September to 1%.

Mortgage interest rates in Switzerland are falling and are currently as low as they were last in 2022, creating attractive financing conditions for borrowers. Moderate economic growth and an inflation rate of around 1.4% are contributing to the attractive interest rate situation. This has led to high demand and stable prices , which further increases the attractiveness of real estate financing.

Forecasts for the coming years are mixed: some analysts expect interest rates to fall due to moderate economic growth, while volatility remains high due to global uncertainties. The SNB will probably continue to ensure price stability and support the economy.

The various mortgage models at a glance

Fixed-rate mortgage

This form of mortgage is characterized by a fixed interest rate that remains unchanged over the entire term. This offers security and predictability, but is not flexible enough to benefit from possible interest rate reductions.

SARON Mortgage

The Saron (Swiss Average Rate Overnight) has replaced the Libor since the end of 2021 and is linked to the short-term money market. The interest rate is adjusted at fixed intervals (usually 3 or 6 months) and consists of the current Saron overnight rate plus an individual margin for the bank. This mortgage is transparent and offers flexibility, but carries the risk of rising interest rates.

Variable mortgage

This mortgage is characterized by a flexible interest rate structure, without a fixed term and with shorter notice periods. As the interest rate is set individually by the banks and is less transparent, this form is often more expensive than fixed-rate mortgages or Saron mortgages.

Libor mortgage (historical)

Until the end of 2021, the Libor rate was a common basis for mortgages. After its abolition, it was replaced by the Saron, which is also influenced by the SNB.

Current interest rates and forecasts

The top rates for a 10-year fixed-rate mortgage were around 1.59% in August 2024, while the Saron mortgage was quoted at around 1.86% including margin. These figures show that fixed-rate mortgages are still a popular option, especially for security-oriented borrowers, while the Saron mortgage offers flexibility for risk-taking customers.

The forecasts for the coming years assume a mixed trend. Although mortgage interest rates are currently low, which may have a positive impact on financing decisions, a slight increase in interest rates cannot be ruled out. Some experts even expect a further slight decline in view of the moderate economic growth. Nevertheless, it remains important to keep a close eye on developments due to global volatility.

At properti, we attach great importance to offering our customers the best conditions for their real estate financing. By working closely with our financial partners, we can offer the best conditions.

Conclusion: Strategies for choosing a mortgage

If you want to benefit from the current low interest rates, you should compare offers and seek independent advice. While fixed-rate mortgages are suitable for stability and long-term planning, the Saron mortgage offers a dynamic option with potential savings. The choice of the right model depends on the individual risk appetite, financial goals and the planned holding period of the property.

It is worth keeping a close eye on developments and, if necessary, considering flexible options such as switch options in order to be able to react to future market changes.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.