Key facts

- Low interest rates promote home ownership: The current low interest rates make the purchase of residential property in Switzerland particularly attractive, as financing costs have fallen and property values continue to rise.

- Opportunity costs as a risk: When buying a home, capital is tied up that could alternatively be invested elsewhere. These opportunity costs should be taken into account when making a decision.

- Tax burdens due to imputed rental value: Property owners in Switzerland must pay tax on imputed rental value as notional income, which increases taxable income. However, mortgage interest can be claimed as a deduction.

Buying a home is not only a lifelong dream for many people, but is also often seen as a valuable form of investment. But to what extent is it really worthwhile to view home ownership as a financial investment? This article examines the opportunities and risks of owning real estate and shows which considerations should play a role in this long-term decision.

Interest rate trends and market conditions: A favorable moment?

Low interest rates are currently making home ownership particularly attractive. Compared to the highs of mid-2022, mortgage interest rates have fallen significantly thanks to monetary policy interventions by the Swiss National Bank(SNB). This means that buyers can secure a property at lower financing costs, making the purchase more attractive as an investment. In the long term, however, it remains unclear whether interest rates will remain this low, which could potentially cause mortgage costs to rise once a fixed interest rate period expires.

Understanding opportunity costs: Capital commitment as a risk factor

Opportunity costs are an important aspect of buying a home. Buying a house ties up capital that could be invested elsewhere. While securities or other investments may offer a higher return, home ownership promises stability and long-term value appreciation. Real estate experts emphasize that although home ownership promises less profit than securities, it offers other advantages such as security and independence from landlords.

Equity and mortgage burden: the influence of financing

If you want to buy your own home, you should secure solid financing . Mortgage interest rates and the required equity ratio of at least 20% of the purchase price are key factors here. Banks also require buyers to be able to afford their mortgage even with a theoretical interest rate of 5% in order to be able to cope with potential interest rate increases. It is therefore important for property buyers to realistically analyze their financial situation in order to minimize potential risks

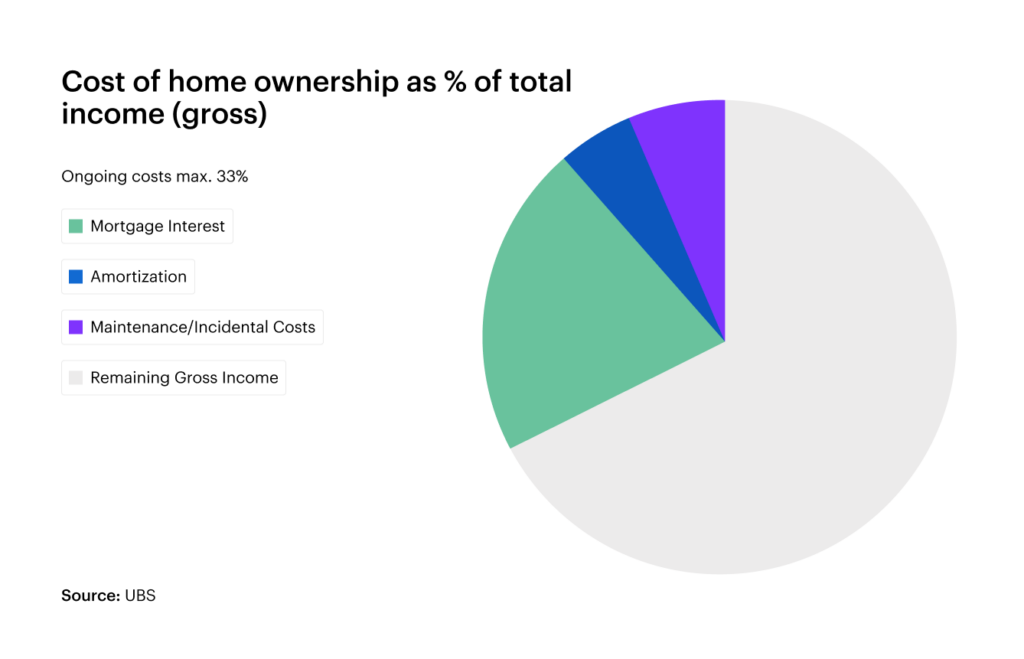

Maintenance and renovation costs: financial provision as an obligation

In addition to financing costs, home ownership also entails ongoing maintenance costs, which are often underestimated. Experts recommend setting aside around 1% of the property value each year for renovations or modernizations. This includes not only minor maintenance, but also major renovations such as energy modernization, which could even become more expensive in the future. In cantons where building insurance is mandatory, its costs should also be included in the planning.

| Canton | Compulsory building insurance | Type of insurance |

| Aargau | Yes | Cantonal buildings insurance |

| Appenzell Ausserhoden | Yes | Cantonal buildings insurance |

| Appenzell Innerhoden | no | Voluntary, except in the Oberegg district, where it is compulsory |

| Basel-Landschaft | Yes | Cantonal buildings insurance |

| Basel-Stadt | Yes | Cantonal buildings insurance |

| Berne | Yes | Cantonal buildings insurance |

| Fribourg | Yes | Cantonal buildings insurance |

| Geneva | no | Voluntary, private insurers responsible |

| Glarus | Yes | Cantonal buildings insurance |

| Grisons | Yes | Cantonal buildings insurance |

| Law | Yes | Cantonal buildings insurance |

| Lucerne | Yes | Cantonal buildings insurance |

| Neuchâtel | Yes | Cantonal buildings insurance |

| Nidwalden | Yes | Cantonal buildings insurance |

| Obwalden | Yes | Compulsory, but via private insurers |

| Schaffhausen | Yes | Cantonal buildings insurance |

| Schwyz | Yes | Compulsory, but via private insurers |

| Solothurn | Yes | Cantonal buildings insurance |

| St. Gallen | Yes | Cantonal buildings insurance |

| Ticino | no | Voluntary, private insurers responsible |

| Thurgau | Yes | Cantonal buildings insurance |

| Uri | Yes | Compulsory, but via private insurers |

| Vaud | Yes | Cantonal buildings insurance |

| Wallis | no | Voluntary, private insurers responsible |

| Zug | Yes | Cantonal buildings insurance |

| Zurich | Yes | Cantonal buildings insurance |

Owner-occupied rental value and tax aspects: The financial balancing act

In Switzerland, property owners must pay tax on the so-called imputed rental value as income. This value, which reflects the benefit of rent-free living, increases the owner’s taxable income, which can be partially offset by deductions for mortgage interest. However, anyone who finances with funds from the pension fund must reckon with a capital disbursement tax. In addition, property gains tax is payable depending on the canton and the length of ownership. These special tax features require precise financial planning in order to keep the burden as low as possible.

Conclusion: well-considered decisions for long-term success

Home ownership can be a worthwhile investment and, above all, offers stability, emotional security and long-term value appreciation – aspects that are harder to find in other financial investments. For many, it therefore represents a valuable alternative to renting. Nevertheless, home ownership should not be viewed purely as a capital investment, as the risks and long-term costs are often underestimated. However, with a critical look at the financing and forward-looking planning, owners can successfully master the property purchase and benefit from the many advantages.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.