|

Getting your Trinity Audio player ready...

|

Key facts:

- The SNB last cut the key interest rate to 0.25% in March 2025, and a further cut to 0.00% is likely in June.

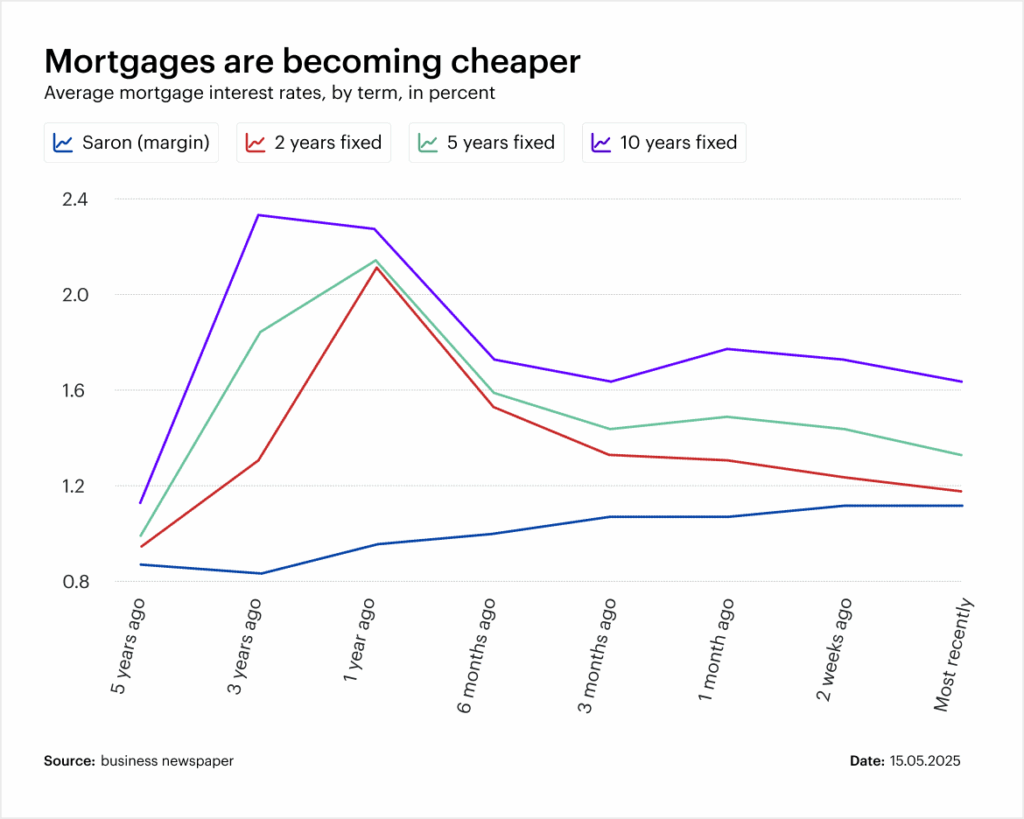

- Ten-year fixed-rate mortgages are currently at around 1.65%, a low since 2022.

- The discussion about possible negative interest rates is back with an impact on demand, prices and sales opportunities.

Mortgage interest rates in Switzerland will remain at a low level in 2025. The Swiss National Bank (SNB) last cut the key interest rate to 0.25% in March – and a further reduction to 0.00% is considered likely next week (June 19), but is not entirely certain. The market expectation: stabilization at a low level. For sellers and owners, this opens up new prospects for financing, sales and reinvestment.

Mortgages 2025: Saron or fixed? The situation on the interest rate market

The trend is clear: mortgage rates are back at a level last seen before the interest rate rise in 2022. Ten-year fixed-rate mortgages currently cost around 1.65%, five-year mortgages in some cases below 1.40%. SARON mortgages are around 1.30-1.60% (incl. margin), with an underlying SARON of 0.2075%.

However, the SNB ‘s expectation to cut interest rates to 0.00% on June 19, 2025 is already largely priced into mortgage rates. This means that there is not much room for downward movement. Instead of further cuts, many institutions expect rates to stabilize, especially for long-term fixed-rate mortgages.

For owners with an expiring mortgage or the intention to sell, it is worth checking now.

The right financing strategy

Fixed-rate mortgage

Particularly interesting for sellers who want to reinvest after selling a property: Fixed-rate mortgages offer interest rate security and planning flexibility. Five to ten-year terms currently cost between 1.35% and 2.00%. The decision depends on the planning horizon: those who want to reinvest capital (e.g. in residential property or renovations) benefit from stability.

SARON Mortgage

SARON products offer flexibility and react immediately to SNB interest rate decisions. They are currently particularly favorable – provided the bank margin remains low. This option can be advantageous for sellers with transitional requirements (e.g. interim financing when relocating), but requires interest rate risk awareness.

Combination of terms

A mix of maturities makes it possible to combine opportunities and hedging. Typical: 50% SARON, 50% fixed-rate mortgage. Anyone planning to buy a new property after selling can thus spread interest rate risks – and remain flexible if market conditions change again.

Regulatory framework: Why Basel III affects financing

In addition to interest rates, regulation plays a decisive role. Basel III makes it more difficult to grant mortgages, as banks have to deposit more equity capital for credit risks. For owners or buyers, this means

- Higher requirements for affordability and own funds

- Stricter review of loan-to-value limits

- Less leeway for special financing (e.g. for refurbishment properties or mixed properties)

This is relevant for sellers : Solid financing with the buyer is becoming a key factor for a smooth sale. The more transparent the buyer’s financing, the lower the risk of delays or abortions in the sales process.

What sellers can do now

Check market value and derive strategy

Whether the sale is planned or only being considered: The current market value is the starting point for every decision. In a low interest rate environment, demand increases – and with it often the achievable price. A professional valuation with up-to-date comparative data is important.

Pre-planning financing solutions

Anyone selling should think about subsequent steps before the notary appointment: reinvestment, renovation, partial sale, passing on as part of an inheritance arrangement. Depending on the scenario, individual financing is required – for example with a mix of maturities or a transitional loan.

Conclusion: Use the low interest rate environment – sell with strategy

Interest rates are low and demand remains solid – a constellation from which sellers can benefit directly. Those who seize the right moment will find it today:

- Buyers with favorable financing

- Investors with a realistic interest rate model

- Banks with competitive offers

At the same time, the scope for further interest rate cuts is limited. Anyone planning should act quickly – with a solid plan and sound advice.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.