Key facts:

- Key interest rate falls to 0.25%: The SNB cuts interest rates again to support the economy.

- Mortgages could become cheaper: SARON rates could fall, while fixed-rate mortgages remain stable.

- New builds remain expensive: Despite low interest rates, Basel III regulations are making construction financing more difficult.

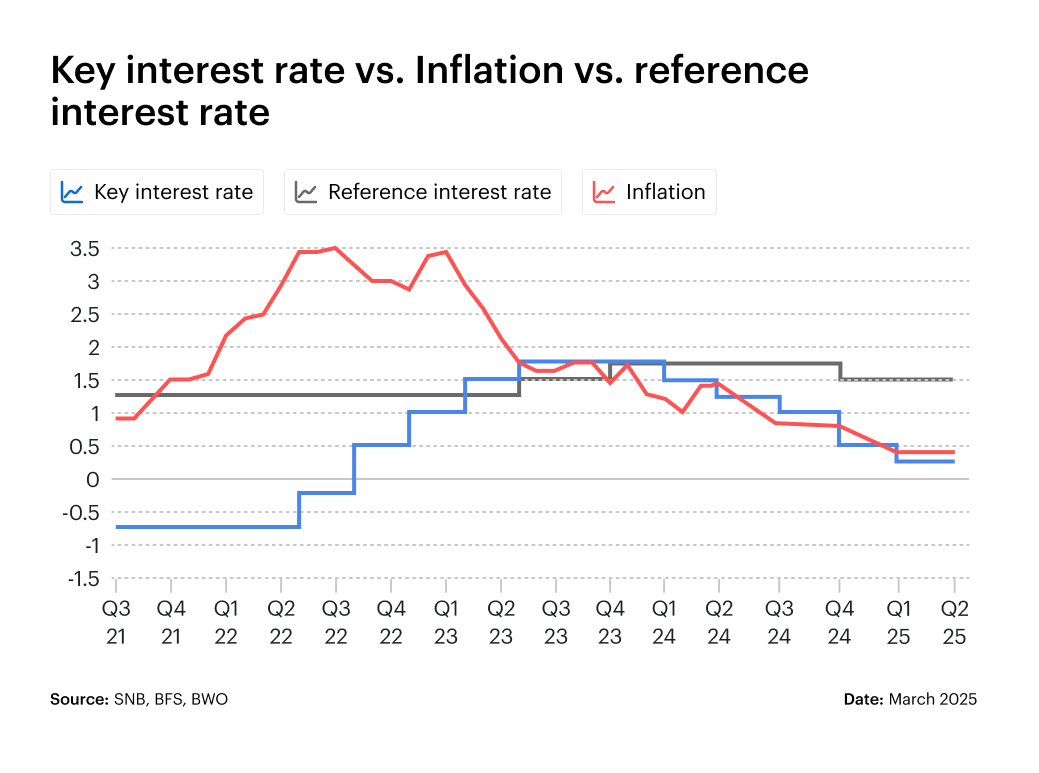

As expected, the Swiss National Bank (SNB) lowered the key interest rate by 0.25 percentage points on March 20. The key interest rate now stands at 0.25%, the lowest level since the post-pandemic rate hike phase. While this measure is aimed at supporting economic development, the impact on the real estate market remains complex.

On the one hand, mortgage borrowers benefit from potentially more favorable financing conditions, but on the other hand, structural challenges remain – particularly with regard to new construction projects and the availability of rental apartments. But how exactly does this decision affect the market and what developments can be expected in the coming months?

Why is the SNB lowering the key interest rate again?

The Swiss economy continues to face challenges such as subdued growth and a difficult global environment. Experts had already predicted an interest rate cut in advance(ZKB forecast), as inflation risks have decreased and the SNB wants to continue to support lending.

Factors that led to the interest rate cut:

- Lower risk of inflation: Price increases in Switzerland have stabilized, in particular due to lower energy prices and continued moderate wage growth.

- Signs of an economic slowdown: GDP growth has slowed, particularly in the construction and industrial sectors.

- International interest rate developments: The European Central Bank (ECB) and the US Federal Reserve have signaled interest rate cuts for 2025. The SNB is adapting to this environment in order to keep the Swiss franc exchange rate stable.

- Objective: To stimulate lending: The reduction to 0.25% is intended to make mortgages and investment loans in particular cheaper in order to stimulate the domestic economy.

Just a few weeks ago, SNB Chairman Martin Schlegel had not ruled out a return to negative interest rates. However, the geopolitical situation has changed. Fiscal policy in Europe is becoming more expansive, particularly in Germany, where additional spending on defense and infrastructure is planned. This has led to rising long-term interest rates, which has reduced the likelihood of negative interest rates in Switzerland.

How does the interest rate cut affect the real estate market?

The impact on the real estate sector varies and depends on several factors – including the reaction of banks, the development of demand and the regulatory framework.

Mortgages: Is financing really getting cheaper?

The interest rate cut is likely to have a particular impact on SARON mortgages, which are directly linked to the prime rate. In the case of fixed-rate mortgages, however, it remains to be seen whether the banks will pass on the lower financing costs in full to customers.

Expert assessment:

- In the short term, variable-rate mortgages in particular could become more favorable.

- In the medium to long term, developments will depend heavily on global monetary policy and inflation.

- Banks could weaken the advantages for customers through stricter lending criteria.

Anyone planning to finance a property should compare mortgage offers carefully and pay attention not only to the prime rate, but also to the individual conditions.

New construction projects: Basel III tightens the financing hurdle

Despite the reduction in interest rates, financing new builds remains challenging. Due to the Basel III regulations, construction loans are considered riskier and are subject to stricter capital requirements.

Consequences for the market:

- Banks are granting building loans more restrictively or demanding higher collateral.

- Without rising real estate prices, many projects will remain unprofitable.

- Residential construction could stagnate, which could lead to a further shortage of supply.

This trend can still be observed – especially in regions with high demand and limited housing supply.

Rental market: easing is a long time coming

Although investors could be relieved by lower interest rates, this will only have an indirect impact on the rental market.

- The reference interest rate will remain stable for the time being, which means that rents are unlikely to fall in the short term.

- Rising construction costs and limited new construction activity could further tighten the supply of rental properties, which could cause rents to rise rather than fall in the long term.

- Investors must weigh up whether the purchase of investment properties remains attractive despite the regulatory hurdles.

The expansionary fiscal policy in Europe is stabilizing the euro-franc exchange rate and reducing deflationary tendencies. This takes pressure off the SNB to make further drastic interest rate cuts. An environment with renewed negative interest rates seems unlikely for the time being.

Short-term relief for tenants is unlikely. In the long term, however, there could be greater demand for alternative housing models, such as shared flats or micro-apartments.

Should you buy or sell a property now?

The decision depends on individual factors. While buyers could benefit from more favorable financing conditions, sellers should keep a close eye on how the market is developing.

When is it worth buying real estate?

- Provided banks pass on the low interest rates to customers and a favorable mortgage is possible.

- If the property has long-term potential, especially in growth regions.

- If alternative forms of investment (e.g. shares or bonds) appear less attractive.

When is a good time to sell?

- If buyers can finance the high real estate prices.

- If the rising real estate prices can be realized.

- If the capital requirement is high or alternative investment options prove to be more lucrative.

Conclusion: Interest rate cut brings opportunities, but also challenges

The renewed interest rate cut to 0.25% could set the real estate market in motion – albeit with different effects. While mortgage borrowers could benefit from cheaper financing, new construction financing will remain challenging. Moreover, direct relief for tenants is not to be expected for the time being.

Investors, buyers and sellers should therefore not only consider the short-term effects of the interest rate cut, but also long-term market developments in their decision-making. While a further interest rate cut to 0.25% has now taken place, there are many indications that this could be the last downward adjustment for the time being. The SNB is likely to act more cautiously in view of international developments. A return to negative interest rates remains unlikely, especially as rising government spending in Europe is raising long-term interest rates and thus influencing the economic leeway of central banks.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.