|

Getting your Trinity Audio player ready...

|

Key facts:

- Only 36% of owners are concerned in detail with affordability in old age.

- 35% of owners used pension fund money for the purchase, with consequences for their pension.

- A sale can create liquidity in old age and reduce fixed costs.

For many owners, their own home is not just a home, but also an important part of their retirement provision. However, new questions arise in retirement: falling incomes, stricter affordability and tax changes due to the imputed rental value can make financing more difficult. Is the mortgage still affordable in old age? If you plan early, you will retain room for maneuver.

Mortgage at retirement age – what does affordability mean?

Affordability describes whether a household can finance the mortgage in the long term. Banks calculate with imputed interest rates of around 4.5-5% – significantly higher than the effective market interest rates. In addition, there are incidental costs of around 1% of the property value per year. Overall, the mortgage may not exceed one third of gross income.

This calculation is often easy for people in employment. At retirement age, however, the income from employment ceases and the AHV and pension fund take its place. As conversion rates fall and pension benefits shrink, affordability becomes more difficult to achieve with the same mortgage volume. Even a mortgage that has remained unchanged for years can suddenly be deemed “unaffordable”.

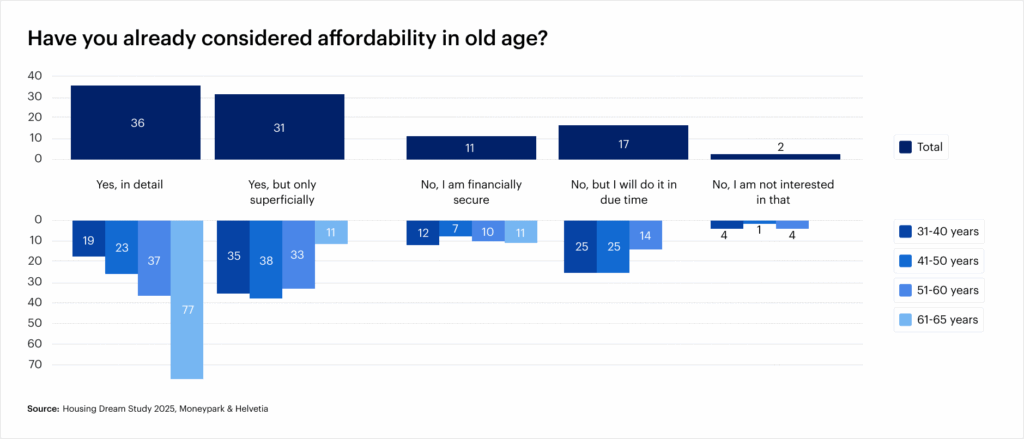

The Dream Home Study 2025 shows: Only 36% of homeowners have considered affordability in old age in detail, while a further 31% have at least considered it superficially. Particularly revealing: awareness increases significantly from the age of 60 – 77% of 61- to 65-year-olds actively address this issue, but only 37% of 51- to 60-year-olds. This makes it clear that many owners are putting off the issue for too long.

Risks: Pension gaps and late amortization

35% of homeowners up to the age of 65 have used pension fund assets to buy a property. This often leaves pension gaps and puts a strain on affordability in old age.

- Pension gaps: Falling conversion rates in pension funds mean that the same amount of capital results in a lower pension. Over the last 20 years, the average conversion rate has fallen from over 7% to around 5% today. This means that anyone who converts CHF 500,000 of capital into a pension will only receive CHF 25,000 per year instead of CHF 35,000.

- Amortization: If the mortgage is amortized late, a high residual debt remains. This increases the fixed costs and reduces the financial leeway in old age.

- Refinancing risk: When a mortgage is extended, the bank reassesses its affordability. If this calculation is negative, the bank can demand a reduction in the debt or refuse to extend the mortgage.

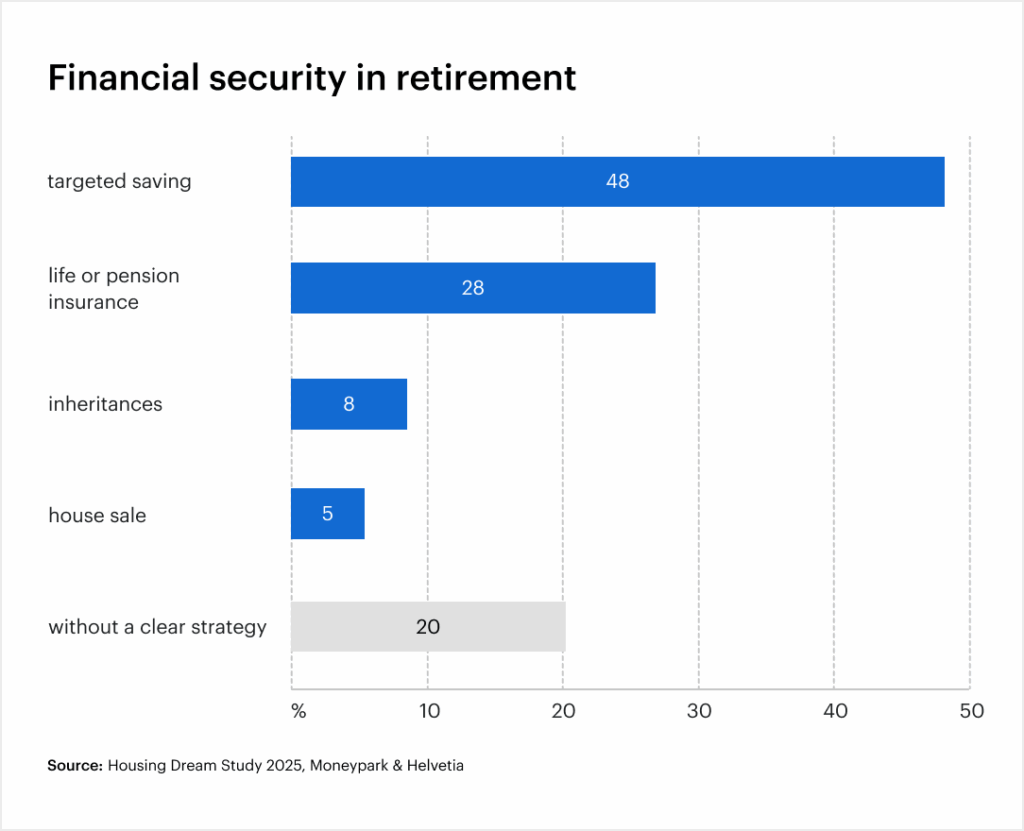

The Wohntraum study adds: while 48% of owners are saving specifically and 28% are using life or pension insurance, 20% have not yet taken any concrete measures. Only 5% are even considering selling their property as a hedge – a sign of how strongly emotional attachment to their home influences planning.

Selling before retirement can make sense: it creates liquidity, reduces fixed costs and enables you to move into a smaller, age-appropriate property.

Imputed rental value and mortgage – tax link

The imputed rental value plays a key role for owners in old age. It is regarded as notional income and is taxed, while at the same time mortgage interest is tax deductible. If the mortgage is reduced or paid off in full, this tax advantage no longer applies, while the imputed rental value remains taxable.

Especially with a view to the vote on September 28, 2025 on the abolition of the imputed rental value. If the imputed rental value is abolished, mortgage interest will lose its deductible character. Owners with high residual debts would be in a worse tax position. For owners of retirement age, this means Financing and tax planning will have to be considered even more closely in future.

Recommendations for action from the age of 50

From the age of 50, it makes sense to take an active approach to pension and mortgage planning. The following steps help to reduce risks:

- Analyze your mortgage: What are the terms? Does an extension at current interest rates (1.4-1.6% for 10-year fixed-rate mortgages, as of summer 2025) make sense?

- Plan amortization: Targeted partial amortization can significantly improve affordability in old age.

- Draw up a pension balance sheet: What pension income is realistic and how high are the monthly fixed costs in old age?

- Consider imputed rental value: Simulate tax scenarios with and without imputed rental value and make possible adjustments to the financing strategy.

- Check the sale: For some owners, selling and moving to a smaller, accessible property may be the more financially sensible solution.

Mortgages and interest rates in late summer 2025

After the SNB cut the key interest rate to 0% in June 2025, mortgages have become significantly cheaper. 10-year fixed-rate mortgages are currently at 1.4-1.6%.

This development offers opportunities, but also harbors uncertainties. Extending now secures low costs, but ties you in for the long term. Those who wait and see risk rising interest rates or changes to the tax framework following the vote on the imputed rental value. Owners should therefore factor both the interest rate market and political developments into their decisions.

Conclusion: Think pension provision and mortgage together

When you reach retirement age, the mortgage is not just a financial issue, but also a strategic one. Affordability, pension gaps, imputed rental value and amortization are all intertwined. The results of the Wohntraumstudie 2025 show that many owners approach the issue late and therefore take risks. Owners who plan in good time and also consider a sale secure room for maneuver and avoid unpleasant surprises.

FAQ

Is it worth selling your property before you retire?

This can make sense if affordability becomes uncertain or high maintenance costs are imminent. Selling before retirement creates liquidity, reduces fixed costs and allows you to move to a smaller, age-appropriate property. The decisive factors are the market environment, tax consequences and personal life planning.

How will the abolition of the imputed rental value affect the mortgage?

If the imputed rental value is abolished, mortgage interest can no longer be deducted for tax purposes. For owners with high residual debts, this means an additional burden, while debt-free owners would be relieved.

Can the bank cancel my mortgage at retirement age?

A current mortgage is not simply terminated. However, if it is extended or adjusted, the bank will reassess its affordability. If this is no longer the case, it can demand a reduction in the mortgage or tighten the conditions.

What happens if the mortgage is no longer affordable in old age?

The bank must then demand a solution – such as a partial amortization, additional collateral or, in extreme cases, a sale of the property. If you act in good time, you can avoid this situation.

Are there special mortgage products for retirees?

Yes, some banks offer special models such as senior mortgages or reverse mortgages where repayment is deferred or offset against the sale proceeds. However, such solutions are often more expensive and should be checked carefully.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.