In recent years, we have seen many changes in the global financial market that have a direct impact on our everyday lives. One of these changes concerns real estate financing and mortgage interest rates in particular. This is not only relevant for financial experts, but also for homeowners and anyone interested in the real estate market.

Understanding mortgages

Many people cannot finance the purchase of a house or condominium or renovations with their savings alone and therefore need a mortgage. The way a mortgage works is basically based on an interest rate and a fixed term. Borrowers pay a monthly installment consisting of interest and repayment of the loan. A mortgage is only granted under certain conditions. The most important of these, in addition to creditworthiness, are equity of at least 20%, which must be contributed, and the affordability of the monthly payments. This is because it often happens that potential buyers have the necessary equity, but forget to work out whether they can actually afford the property on a day-to-day basis.

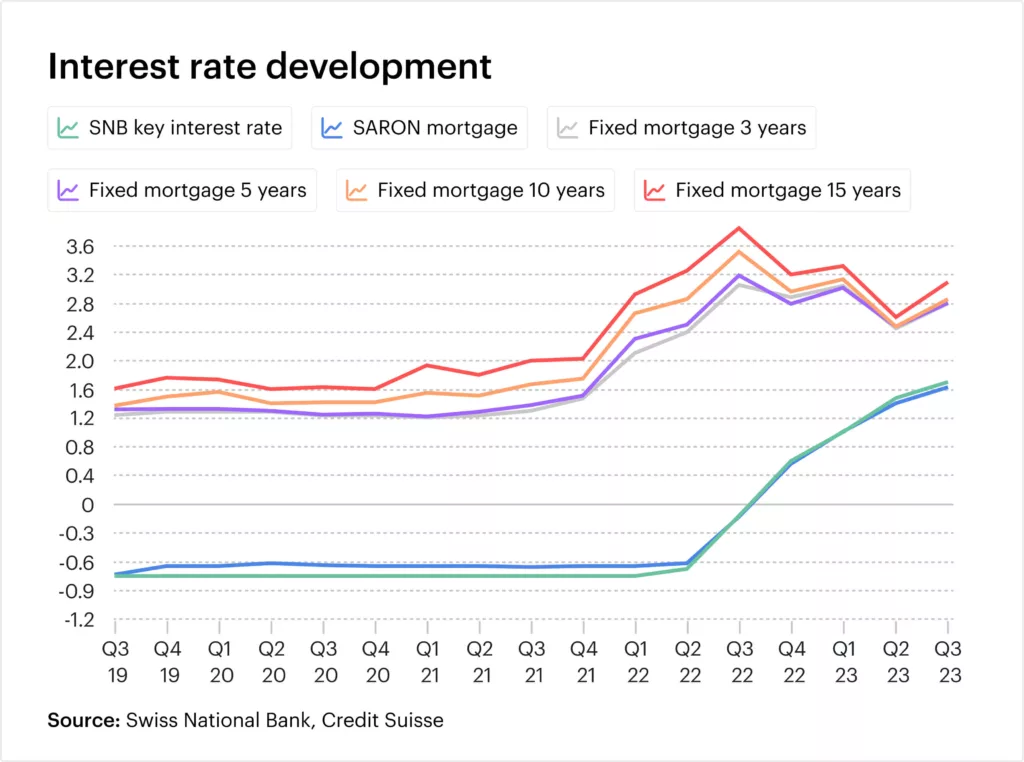

In summary, there are two types of mortgage in Switzerland: fixed-rate mortgages with terms of 2 to 15 years and the SARON mortgage, which is based on the SNB key interest rate and adjusts variably to the market.

The SNB’s key interest rate influences the conditions at which banks can offer loans. In principle, quarterly increases or decreases are passed on directly to the borrower. Falling borrowing costs are therefore an incentive for potential buyers to invest in the real estate market and buy their own property. On the other hand, higher interest rates lead to increasing financial risks and, in the case of buy-to-let properties, to lower profitability as cash flow is reduced.

Strategies for a profitable mortgage

As a property owner, it is advisable to prepare for possible financial changes. Because even a few percentage points can make a significant difference in interest rates over the years, diversification of the real estate portfolio is recommended for real estate investments in order to minimize any risks.

Table for assessing the right choice of financing:

Source: UBS

Long-term perspective and adaptability

When investing in real estate, it is crucial to take the interest rate risk into account. As we have seen in recent months, an unexpected rise in interest rates can have a significant impact on financing costs and therefore the profitability of an investment. This could potentially cause financial difficulties for first-time buyers and refinancers in particular. A long-term investment strategy with flexibility can counteract such risks. In addition, a long-term approach makes it possible to observe market developments and react to changes without being driven by short-term market volatility.

Continuous monitoring of interest rates, such as the prime rate and mortgage rate, is recommended. By making timely adjustments, whether by rescheduling or restructuring the financing, investors can prevent undesirable cost increases and benefit from more favorable conditions in a changing interest rate environment.

Conclusion

Real estate financing is an important topic for all existing and potential property owners, and sound specialist knowledge is crucial for making the right decisions. It is important to keep an eye on market trends and interest rates, especially in view of the rapid changes in recent months. Therefore, plan ahead for a future-proof investment and consult experts at an early stage for a successful real estate strategy.

All data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.