Key facts:

- In the event of a divorce, forms of ownership and matrimonial property regimes are decisive for the division of residential property.

- Tax aspects such as property gains tax, imputed rental value and debt interest deduction should be taken into account.

- Early advice from experts helps to find fair and sustainable solutions.

Divorce not only brings with it emotional challenges, but also raises important questions about joint home ownership. In addition to the psychological strain, legal, financial and tax aspects need to be clarified.

Matrimonial property regimes and forms of ownership in Switzerland

In Switzerland, the division of assets in the event of divorce is governed by the Swiss Civil Code (ZGB). The three matrimonial property regimes determine how the joint assets are distributed:

- Participation in acquired property: The standard matrimonial property regime without a marriage contract: assets acquired during the marriage are divided, while personal property (e.g. inheritances) remains with the respective spouse.

- Separation of property: Assets remain strictly separate; each partner retains their own property. This arrangement requires a marriage contract.

- Community of propertyJoint marital property is owned jointly by both partners and is divided in the event of divorce. Details are set out in the marriage contract.

Specific rules on the division of assets also apply to cohabiting couples, as they are not covered by the matrimonial property regimes of the Swiss Civil Code. Here it is important to make contractual agreements to avoid disputes. Further details on this topic can be found in the blog “Property in a cohabiting couple”.

In addition to the matrimonial property regimes, the forms of ownership also play a decisive role in dealing with residential property.

- Sole ownership: If the property belongs to one spouse alone, it remains in their possession even after the divorce.

- Co-ownership: Both spouses are entered in the land register with certain shares. These shares can be different and are regulated accordingly in the event of a divorce.

- Joint ownership: The property belongs to both partners jointly, without fixed shares. Decisions about the property must be made jointly.

What to do with the shared property?

Various options are available depending on the individual situation and agreement:

1. sale of the property

The property is sold and the proceeds, after deduction of liabilities, are divided according to the ownership shares. This is a pragmatic solution, especially if neither partner can or wants to finance the property alone. However, property gains tax may be payable.

2. takeover by a spouse

One spouse takes over the property and pays the other spouse’s share accordingly. In this case, the financing bank must check whether the remaining partner can bear the mortgage alone. This solution does not lead to immediate taxation of the property gain, as it is considered a tax-deferred sale.

3. continuation of the joint ownership

If the partners keep the property, for example to rent out. A written agreement on the management and division of income and running costs must be agreed.

4. transfer free of charge

In rare cases, one of the spouses remains living in the property free of charge while the other keeps their share. This arrangement is stipulated in the divorce decree and is particularly suitable if children are involved.

What happens to a joint mortgage?

A joint mortgage requires clear arrangements in the event of a divorce. The following scenarios are possible:

- Division of the mortgage: In rare cases, the mortgage is split between both partners. This is complex and requires an amendment to the mortgage agreement.

- Repayment by sale: The mortgage is repaid with the proceeds of the sale. The remaining proceeds are divided up.

- Takeover by a partner: A partner takes over the entire mortgage. This requires the bank’s consent.

Tax aspects of a divorce

The tax consequences of a divorce depend heavily on the solution chosen for the property. When the property is sold, property gains tax is usually levied, which varies depending on the canton and the amount of the gain. If one spouse remains in the property, they must pay tax on the imputed rental value as income. In addition, debt interest can be claimed for tax purposes depending on the ownership structure and use of the property. These factors should be taken into account when making a decision in order to avoid financial disadvantages.

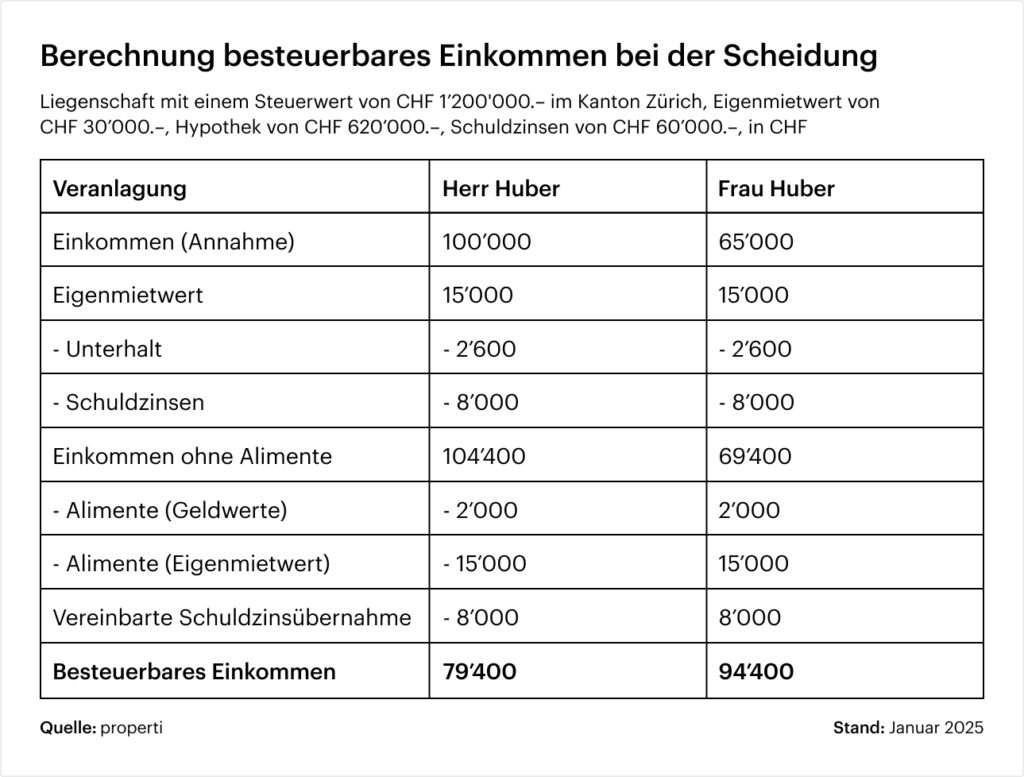

Example for clarification

Mr. and Mrs. Huber own a joint property with a tax value of CHF 1,200,000 and a mortgage of CHF 620,000. Mrs. Huber remains living in the house for the time being, while Mr. Huber assumes the debt interest of CHF 16,000 and pays monthly alimony of CHF 2,000. This arrangement affects both the property and income tax of both partners.

Conclusion

The settlement of residential property in the event of divorce requires careful planning and advice. In addition to legal aspects, tax consequences should also be considered. Involving experts such as lawyers and financial advisors at an early stage can help to find a fair and viable solution for both parties.

Note: This article is for general information purposes only and does not replace individual legal advice.

Data are without guarantee. The information on these Internet pages has been carefully researched. Nevertheless, no liability can be assumed for the accuracy of the information provided.